CCUS growth key to IEA Net-Zero Emissions (NZE) reductions targets

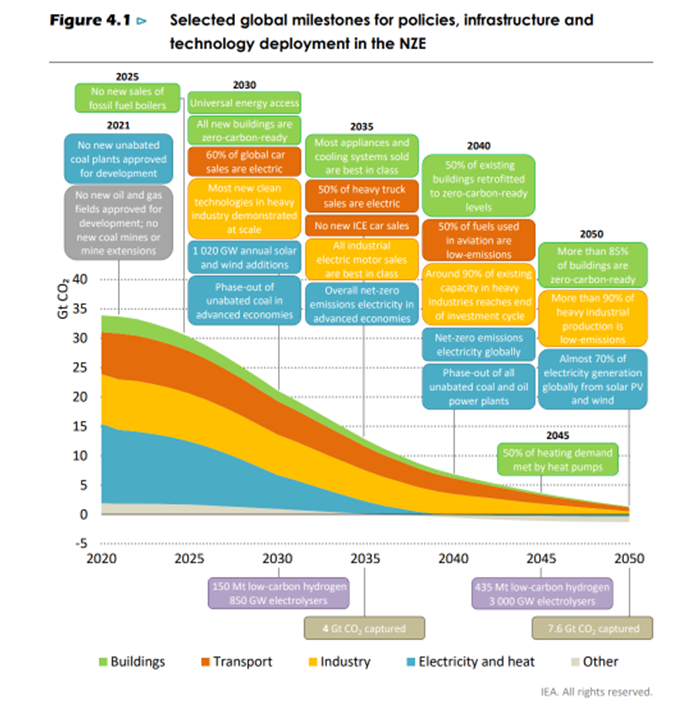

In its Net Zero Emissions by 2050 (NZE) scenario report, the International Energy Agency (IEA) lays out over 400 milestones on the path to achieving net zero emissions by 2050 in order to retain a “fighting chance,” staving off the worst effect of climate change while providing universal access to energy services and improving air quality. Two of the 27 milestones highlighted in Figure 4.1 from the report deal with carbon capture, utilization, and storage (CCUS), which the IEA estimates must increase 100-fold above current levels to 4 gigatonnes of CO2 per year (GtCO2/yr) by 2035, further rising to 7.6 GtCO2/yr by 2050. This would require new investment on the order of $160 billion (US, 2019) over the next three decades.

The NZE report effectively demonstrates that investment in CCUS is not only compatible with ramped-up investment in energy efficiency and renewable energy (EE/RE) objectives, but a complementary and essential partner to them on the path to net zero. Although the 7.6 GtCO2/yr of emissions reductions by 2050 from CCUS account for around 15% of the 50 GtCO2/yr of gross reductions needed to reach net-zero emissions that year, the commensurate $160 billion annual investment in CCUS would account for only 3.6% of the $4.5 trillion/year needed across all technologies. This is largely due to the NZE’s low reliance on CCUS to attain its policy goals.

The two largest NZE emissions reductions are from the $1.1 trillion annual investment made in the transportation sector, such that electricity, hydrogen, and biofuels account for nearly 90% of all transportation energy demand in 2035 (a reverse from present-day, in which 90% of demand is satisfied by oil products), and $2 trillion invested each year in the electricity generation and grid expansions needed to rapidly increase electrification and reduce fossil fuels to 7% of world power generation. Rather than competing with these technologies, CCUS grows alongside them. It proves a deciding factor in the energy sector keeping its net emissions at or below 460 GtCO2 through 2050 to ensure the world remains within its 500-GtCO2 “carbon budget” needed to retain a 50% chance of limiting emissions to 1.5 degrees Celsius ( ͦC).

The NZE is one of four World Energy Outlook (WEO) models that the IEA developed using its World Energy Model (WEM). Its 1.5 ͦC rise above pre-industrial temperatures (compared to about 1.25 ͦC today) through 2100 would still likely cause a 45% increase in extreme heating events worldwide and a 20% increase in drought frequency. However, this is relatively benign compared to the 2.6 ͦC rise under the stated energy policies (STEPS) scenario, in which governments do not implement announced climate pledges. Under STEPS, the frequency of extreme heating events doubles (with each event more than twice as intense on-average), and ecological droughts are 40% more frequent (with each drought twice as intense on-average).

The WEM replicates how energy markets function around the world. Its projections combine technical and economic parameters for each technology in its Energy Technology Perspectives (ETP) model with financial and policy assumptions. The NZE uses these inputs to simulate the percentage of emissions reductions from each technology type. Of the 7.6 MtCO2/yr of reductions through 2050 from CCUS, some 55% come from industries like cement or biomass where the technology is in the demonstration or prototype phase. However, similar uncertainties exist for other technologies, like electrification (30% of all reductions from prototype/demonstration-phase technologies), bioenergy (45% from prototype/demonstration-phase technologies) and hydrogen (> 75% from prototype/demonstration-phase technologies).

There is additional uncertainty surrounding the half of all CCUS reductions coming from large-scale implementation with fossil fuel-producing energy and industrial applications. To account for this, the IEA runs a low-CCS (LCC) case in the WEM, in which there are no new CCUS projects to capture, transport, and store CO2 emissions from fossil fuel producers. This would require an additional 11,300 terawatt-hours (TWh) each year of electricity from carbon-free sources that would backfill for CCUS reductions in the NZE rather than contributing to its overall reduction targets. It would also require 11,400 TWh of carbon-free generation that would serve the same purpose in the industrial sector, where it would provide 2,400 TWh to backfill CCUS reductions there with electric equipment in industries like cement and refining equipment (assuming they could be deployed at-scale) and 9,000 TWh for additional “green hydrogen” (both for this process, and to replace blue hydrogen from plants equipped with carbon capture in the NZE). These investments would add a cumulative $15 trillion to the cost of achieving NZE goals, several times more than the $650 billion in cumulative savings from not equipping power and manufacturing plants with CCUS, and equal to three years of total NZE spending on-average!